Owning a vehicle is a significant journey, not just a purchase. For most, it represents a substantial investment and a key part of their financial health. Whether you dream of a custom-built car tailored to your exact specifications or cherish a timeless American classic, managing this investment wisely is crucial.

We understand the complexities of automotive personalization and the entire ownership lifecycle. Strategic financial planning can make a big difference. This guide will help you navigate these choices.

We will explore how initial decisions, such as custom ordering your vehicle from trusted sources like Kruse custom ordering, can maximize value. More importantly, we will delve into refinance car loan rates. Understanding these rates can optimize your vehicle’s financial journey and potentially save you a lot of money over time.

In today’s automotive landscape, the option to custom order a vehicle offers a distinct advantage. Instead of settling for what’s available on the lot, you can specify everything from the engine and transmission to interior finishes and advanced safety features. This process ensures that the vehicle you drive perfectly matches your needs and preferences, straight from the factory. It’s about building a vehicle to your exact specifications, ensuring that every detail aligns with your vision. This approach also helps manage inventory more efficiently for dealerships, as vehicles are often built to confirmed customer orders.

Maximizing Value through Custom Vehicle Ordering

Choosing a direct-to-consumer or custom order approach can significantly maximize the long-term value of your vehicle. By carefully selecting features that are important to you and will appeal to future buyers, you can enhance its resale value. This isn’t just about luxury; it’s about practical choices that align with market demand. For instance, opting for popular technology packages or fuel-efficient powertrains can make your vehicle more attractive down the line. Furthermore, with custom orders, you benefit from the full manufacturer’s warranty from day one, covering your bespoke features and ensuring peace of mind.

Long-term Financial Planning for Custom Vehicle Ordering

When considering a custom-ordered vehicle, it’s essential to think about the long-term financial implications. The initial investment might be higher due to specialized features, but this can be offset by a potentially slower depreciation curve if the customizations are desirable. Effective budgeting and understanding the initial interest rates on your auto loan are paramount. Planning for the total cost of ownership, including insurance, maintenance, and potential future financing options, helps ensure that your dream vehicle remains a financially sound decision throughout its life.

Optimizing Your Investment: Understanding Refinance Car Loan Rates

Managing your vehicle’s financing doesn’t end after the initial purchase. In fact, many drivers find significant savings by strategically refinancing their car loans. Auto loan refinancing involves replacing your existing car loan with a new one, ideally with more favorable terms. This could mean a lower interest rate, a different repayment schedule, or reduced monthly payments.

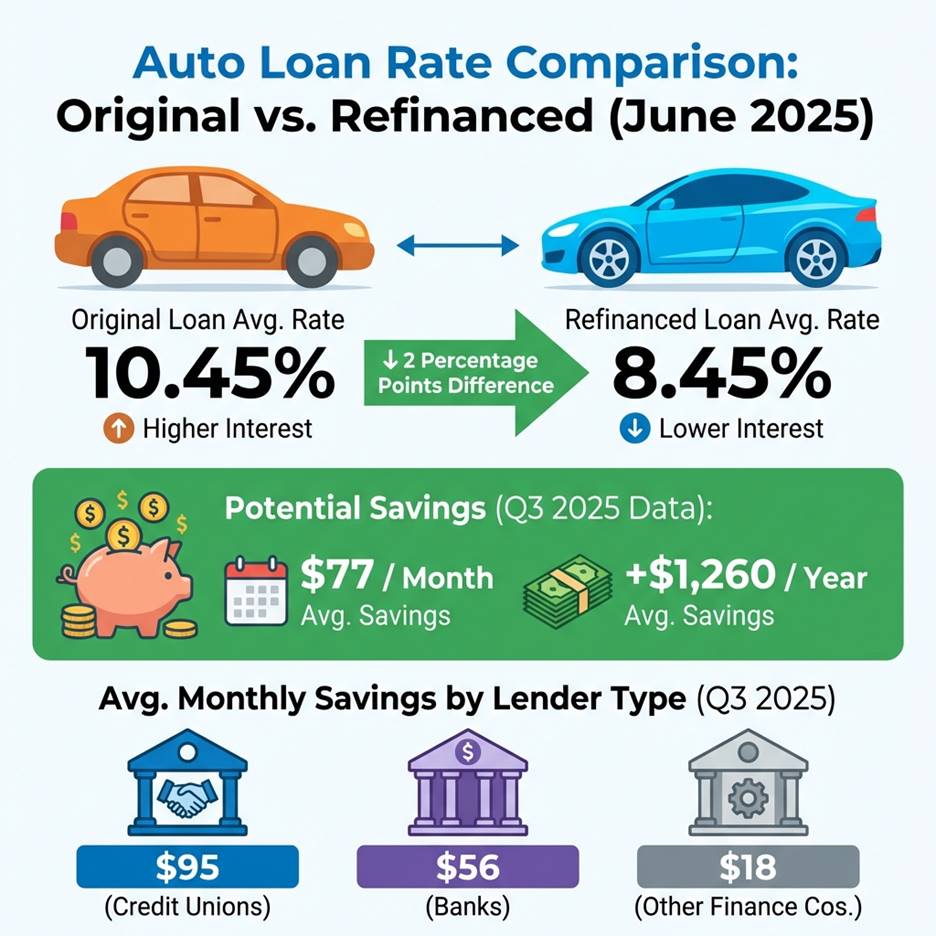

Recent data underscores the power of refinancing. The average rate for refinanced auto loans stood at 8.45% in June 2025, which is a notable 2 percentage points lower than the average 10.45% rate borrowers were paying before refinancing. This translates to substantial savings for many. Car owners who refinanced reduced their interest rate by an average of 2.08% in Q3 2025, leading to average monthly payment savings of $77. Over a year, this could amount to an average of +$1,260 in savings, as seen by platforms like SafeLend.

It’s also worth noting the difference between lenders. Credit unions, for example, provided average monthly payment savings of $95 for refinanced auto loans in Q3 2025, compared to $56 for banks and $18 for other finance companies. Major financial institutions like TD Auto Finance and Scotiabank also offer competitive options, with terms potentially extending up to 96 months and loan amounts up to $200,000 for eligible vehicles. These figures highlight the importance of exploring your options and not settling for your initial loan terms.

When to Refinance a Car Loan

Deciding when to refinance your car loan is a strategic decision that can significantly impact your financial health. Several scenarios make refinancing a smart move:

- Market Interest Rates Have Dropped: If general interest rates have declined since you first took out your loan, you might qualify for a lower rate now. Keeping an eye on broader economic trends can help you seize these opportunities.

- Your Credit Score Has Improved: A higher credit score signals lower risk to lenders, often qualifying you for better interest rates. If you’ve been diligent with payments and your score has risen, it’s an excellent time to explore refinancing.

- You Want Lower Monthly Payments: If your financial situation has changed, or you simply want more breathing room in your budget, refinancing to a longer loan term can reduce your monthly payments. Be mindful, however, that extending the term may increase the total interest paid over the life of the loan.

- To Remove or Add a Co-Signer: If a co-signer was necessary for your initial loan but your credit has since improved, refinancing can allow you to remove them. Conversely, if adding a co-signer would help you secure a better rate, refinancing provides that opportunity.

- You Want to Switch Lenders: Perhaps you’re dissatisfied with your current lender’s service, or you’ve found a new lender offering more attractive terms or benefits. Refinancing allows you to move your loan.

A good rule of thumb is to consider refinancing if you can reduce your interest rate by at least 1%. This threshold generally ensures that the savings outweigh any potential fees or administrative costs associated with the new loan.

Benefits and Potential Drawbacks of Refinancing

Refinancing a car loan offers several compelling benefits, but it’s also crucial to be aware of potential drawbacks.

Benefits:

- Lower Interest Rate: This is often the primary goal, leading to significant savings on the total cost of your loan.

- Reduced Monthly Payments: By securing a lower interest rate or extending your loan term, you can free up cash flow in your monthly budget.

- Save Money on Total Interest Paid: Even a small reduction in interest rate can lead to substantial savings over the life of the loan.

- Change Loan Term: You can shorten your loan term to pay it off faster (and save on interest), or lengthen it to reduce monthly payments.

- Remove a Co-Signer: If your credit has improved, you can refinance to remove a co-signer from the loan.

- Cash-Out Refinance: In some cases, you can borrow more than you owe on the car, accessing equity for other financial needs.

Potential Drawbacks:

- Increased Total Interest (with longer terms): While extending the loan term lowers monthly payments, it almost always means you’ll pay more in total interest over the life of the loan.

- Prepayment Penalties: Some original loan agreements include penalties for paying off the loan early. Always check your current loan terms to see if this applies, as it could negate the benefits of refinancing.

- Negative Equity: If you owe more on your car than it’s currently worth (known as being “underwater” or having negative equity), refinancing can be difficult, as lenders are hesitant to lend more than the vehicle’s value.

- Fees: New loans can come with origination, administrative, or title transfer fees. Factor these into your savings calculations.

- Impact on Credit Score: A hard credit inquiry for the new loan can temporarily ding your credit score. However, consistent on-time payments on a lower-interest loan can improve your score over time.

Carefully weighing these factors against your financial goals is essential before proceeding with a refinance. For more insights on the mechanics of refinancing, Experian provides a detailed overview of auto loan refinancing options and rates.

Navigating the Refinancing Process for Custom and Classic Cars

Refinancing a car loan, whether for a custom-ordered vehicle or a cherished classic, involves a structured process. Lenders will evaluate both your financial profile and the vehicle itself. A strong credit score is paramount; generally, a score above 700 is considered good and can help you qualify for the best rates. Lenders also look at your debt-to-income (DTI) ratio to ensure you can comfortably manage the new payments.

Vehicle eligibility is another key factor. While policies vary, many lenders have restrictions on the age and mileage of the vehicle they will refinance. Common limits include vehicles being no older than 10 years or having no more than 100,000 miles. However, some specialized lenders might be more flexible, especially for classic cars with appreciating value. Loan terms can be quite flexible, with options extending up to 96 months, and loan limits can reach up to $200,000, as seen with some major Canadian banks.

Step-by-Step Guide to Securing a New Loan

The process of refinancing your car loan can be broken down into several manageable steps:

- Review Your Current Loan: Gather all the details of your existing loan, including your current interest rate (APR), the remaining balance, the number of months left, and any prepayment penalties.

- Determine Your Vehicle’s Value: Use reputable valuation tools like Kelley Blue Book or Edmunds (for US vehicles) or Canadian equivalents to estimate your car’s current market value. This helps determine if you have positive equity.

- Check Your Credit Score: Obtain a copy of your credit report and score from major credit bureaus like Equifax or TransUnion. Knowing your score helps you understand what rates you might qualify for. You can often check your credit score for free through services provided by the Canadian government.

- Compare Lenders and Loan Offers: This is a crucial step. Don’t just go with the first offer. Shop around and compare offers from various lenders, including banks, credit unions, and online lenders. Websites like NerdWallet or WalletHub offer comparison tools that can help you find competitive rates. Many lenders offer pre-qualification with a “soft” credit check, which doesn’t impact your score, allowing you to gauge potential rates.

- Apply for Refinancing: Once you’ve chosen a lender, complete their application. Be prepared to provide detailed financial and vehicle information.

- Finalize the New Loan and Title Transfer: After approval, you’ll sign the new loan documents. The new lender will then pay off your old loan, and the vehicle’s title will be transferred to reflect the new lienholder.

Required Documentation for a Successful Application

To ensure a smooth refinancing process, have all your documents in order. While requirements may vary slightly by lender, you’ll generally need:

- Proof of Income: Recent pay stubs (typically for the last 3 months), tax data (like T4s in Canada), or bank statements showing consistent income.

- Personal Identification: A valid driver’s license and proof of residence.

- Vehicle Information: Your vehicle’s insurance policy, registration, and Vehicle Identification Number (VIN).

- Current Loan Details: Your existing loan contract, including the payoff amount and lender contact information.

Having these documents ready will expedite your application and move you closer to securing a better car loan rate.

Advanced Financial Strategies for Vehicle Owners

Beyond simply lowering your interest rate or monthly payment, refinancing can open doors to more advanced financial strategies for vehicle owners. Understanding these options can help you leverage your vehicle’s equity and manage your overall debt more effectively.

One such strategy is a cash-out refinance. If your vehicle has significant equity (meaning it’s worth more than you owe), some lenders may allow you to borrow more than your current loan balance. The difference is given to you as cash, which you can use for various purposes, such as debt consolidation (paying off higher-interest credit card debt), home improvements, or other major expenses. While this can provide immediate liquidity, it’s important to weigh the risks, as you’re increasing your car loan amount and potentially extending the repayment period.

Alternatively, if you’re struggling with payments but don’t want to refinance, a loan modification might be an option. This involves working directly with your current lender to alter the terms of your existing loan, such as temporarily reducing payments or extending the term. This is typically considered a last resort to avoid default.

For those considering a change, exploring trade-in alternatives or leasing options can also be beneficial. If your vehicle no longer meets your needs, selling it privately or trading it in could provide a down payment for a new purchase or lease.

Impact of Refinancing on Credit Scores

Any time you apply for new credit, there’s an impact on your credit score. When you apply for a car loan refinance, lenders perform a “hard inquiry” on your credit report. This type of inquiry can temporarily lower your credit score by a few points, typically for a short period. However, the overall impact is usually minor and short-lived, especially if you have a strong credit history.

The long-term effects of refinancing are often positive. By securing a lower interest rate and more manageable payments, you’re more likely to make on-time payments, which is the most significant factor in maintaining a healthy credit score. Furthermore, a new loan can diversify your credit mix, which can also be beneficial. To minimize the impact of multiple inquiries, it’s advisable to do all your rate shopping within a short window (typically 14-45 days), as credit bureaus often count multiple inquiries for the same type of loan within that period as a single inquiry.

Comparing Lenders and Shopping Around

To truly optimize your refinance car loan rates, comparing offers from different lenders is non-negotiable. The market is competitive, with various institutions offering different rates, terms, and benefits.

- Online Platforms: Many online lenders specialize in auto loan refinancing and offer quick pre-qualification processes. Sites like AutoLoanRate.com allow you to compare daily rates and terms from multiple providers.

- Local Banks and Credit Unions: Don’t overlook traditional banks and local credit unions. Credit unions, in particular, are known for offering competitive rates and personalized service, often resulting in greater monthly savings for refinanced loans.

- Dealership Networks: While dealerships are primarily for new purchases, some also facilitate refinancing through their network of lenders.

- Your Current Lender: It’s worth checking if your current lender offers refinancing options, as they might provide a loyalty discount or streamlined process. However, always compare their offer with others.

When comparing, look beyond just the interest rate. Consider the total cost of the loan, including any fees, and the flexibility of the terms. Many lenders offer autopay discounts (e.g., 0.25% to 0.50% off your APR) for setting up automatic payments. Utilizing pre-qualification tools, which typically use a “soft” credit pull, allows you to see potential rates without affecting your credit score, making the shopping process much more efficient.

Frequently Asked Questions about Custom Vehicle Ordering and Financing

As we navigate custom vehicles and financial optimization, several common questions often arise.

Can you refinance a car loan with bad credit?

Yes, it is possible to refinance a car loan with bad credit, but it comes with specific considerations. While traditional lenders might offer higher rates or reject applications, specialized lenders and subprime auto finance companies often cater to borrowers with less-than-perfect credit. The key is demonstrating an improved financial situation since your original loan, such as consistent on-time payments, a reduction in other debts, or an increase in income. You might not get the lowest rates, but even a slight reduction can lead to savings. Some lenders may require a waiting period, often 6-12 months of on-time payments, before considering a refinance for those with bad credit.

How soon after getting an original car loan can you refinance?

The timing for refinancing can vary. Some lenders have “seasoning requirements,” meaning they prefer you to have made a certain number of payments (e.g., 3-6 months) on your original loan before they’ll consider refinancing. This allows them to see a payment history. However, if you secured a high-interest loan initially and your credit score has significantly improved almost immediately, or if you were simply marked up by a dealership, some lenders might allow you to refinance much sooner, even within a few weeks. The main hurdle in such cases might be the time it takes for your original lender to process the title and for the new lender to complete their paperwork. Always check with potential new lenders about their specific policies.

Are there prepayment penalties or fees to watch out for?

Yes, it’s crucial to be vigilant about prepayment penalties and various fees when considering refinancing.

- Prepayment Penalties: Some original loan agreements include a clause that charges you a fee if you pay off your loan early. This penalty is typically a percentage of the outstanding balance (e.g., 2%) or a set number of months’ interest. However, many jurisdictions, including some in Canada and the U.S., have regulations limiting or prohibiting these penalties, especially on longer-term loans (e.g., loans with terms of 61 months or longer often cannot have prepayment penalties). Always review your current loan contract carefully.

- Origination Fees: These are fees charged by the new lender for processing your loan.

- Administrative Costs: These can include fees for title transfers, lien recording, or other paperwork.

While these fees exist, the overall savings from a lower interest rate often outweigh them. It’s essential to calculate the total payback of the new loan, including all fees, and compare it to the remaining total cost of your current loan to determine if refinancing is truly beneficial. Transparency from the new lender about all costs involved is a good sign.

Conclusion

The journey of vehicle ownership, from the excitement of a custom order to the pride of maintaining an American classic, is filled with decisions that impact both your driving experience and your financial well-being. By understanding the strategic advantages of tailoring your vehicle to your exact specifications and then actively managing its financing through informed refinancing, you empower yourself to make the most of your investment.

Strategic refinancing, driven by factors like improved credit, declining market rates, or a need for adjusted payments, can lead to substantial savings and enhanced financial flexibility. We encourage you to continuously monitor market conditions, evaluate your credit health, and compare offers from various lenders to ensure you’re always securing the best possible terms. Informed ownership is smart ownership, allowing you to enjoy your vehicle while maintaining robust financial health.

{kind=link}